Picture this scenario: your organisation has spent three years building sophisticated applications on a major cloud platform, integrating deeply with proprietary services that seemed like brilliant shortcuts at the time. Then your cloud provider announces a 40% price increase, or worse, discontinues a critical service your business depends upon. Suddenly, those convenient vendor-specific features feel more like digital handcuffs than technological advantages.

This predicament has haunted cloud adoption since the industry’s early days, but 2025 marks a pivotal moment in the vendor lock-in narrative. A perfect storm of regulatory intervention, technological maturation, and shifting enterprise priorities is fundamentally reshaping the balance of power between cloud providers and their customers. For the first time since public cloud emerged, organisations have genuine alternatives to single-vendor dependency and the tools to implement them successfully.

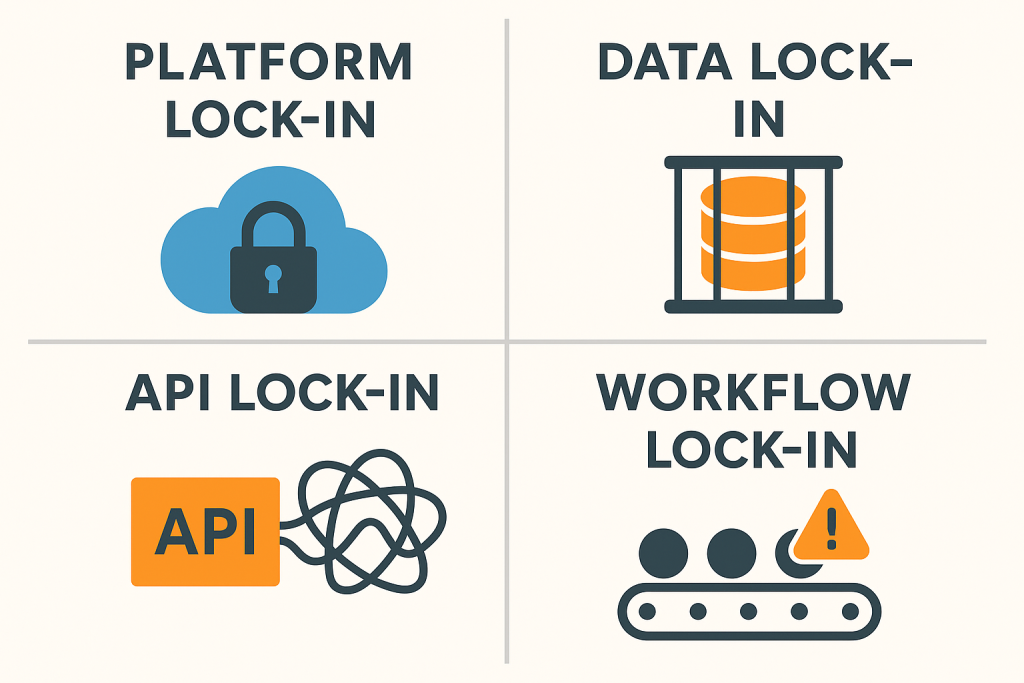

The Modern Face of Vendor Lock-in

Cloud vendor lock-in has evolved far beyond simple contractual obligations into a sophisticated web of technical, economic, and operational dependencies. Think of it as digital quicksand: the more deeply embedded an organisation becomes, the more difficult and expensive extraction becomes.

Platform lock-in represents the most visible challenge. Cloud service providers have developed increasingly sophisticated strategies to retain customers through proprietary services that resist standardisation. AWS Lambda’s serverless functions, Azure’s Active Directory integration, and Google Cloud’s AI Platform demonstrate how providers create genuinely innovative capabilities that simultaneously deliver value and establish dependency.

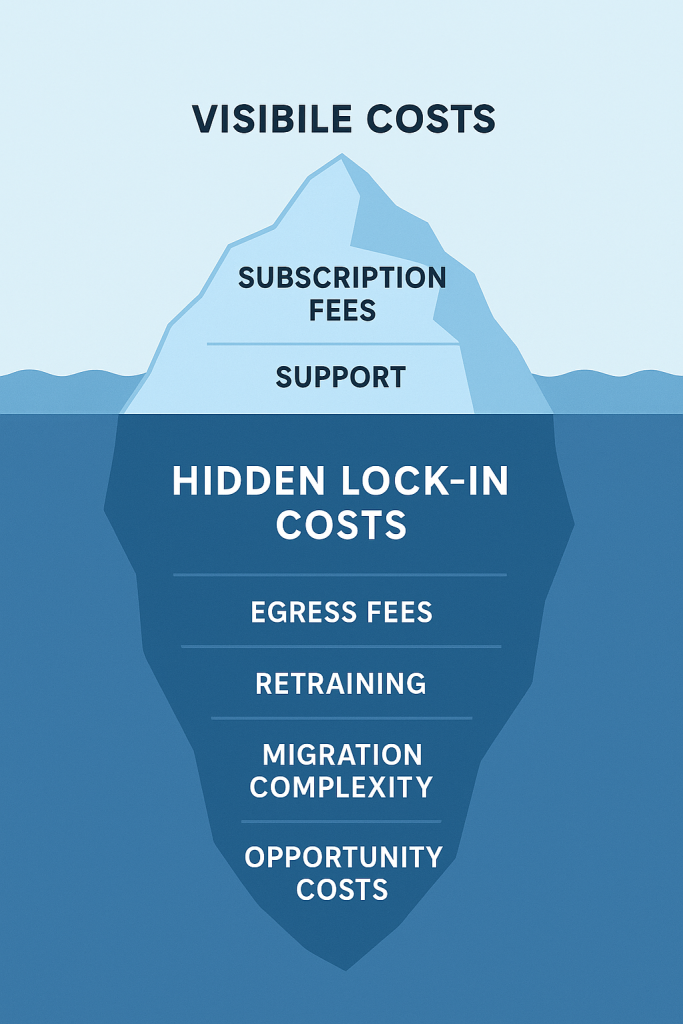

Data lock-in poses perhaps the most insidious barrier. Beyond the notorious egress fees, which historically marked up data transfer costs by approximately 80 times compared to actual bandwidth expenses, organisations face format incompatibilities and transfer limitations that can make migration practically impossible. Consider Amazon DynamoDB’s proprietary data models or Azure Cosmos DB’s custom APIs: these services create lasting dependencies that extend far beyond storage costs into the very architecture of applications.

The subtler challenge of API lock-in creates coding dependencies that require significant development resources to overcome. Each provider’s authentication models, service endpoints, and integration patterns become embedded in application architecture, transforming migration from a simple infrastructure change into a comprehensive redevelopment exercise.

Workflow lock-in emerges through deployment pipelines, monitoring systems, and operational procedures that become deeply integrated with provider-specific tools. Those elegant AWS CloudFormation templates and Azure Resource Manager configurations represent infrastructure-as-code investments that resist portability despite their apparent flexibility.

The Hidden Economics of Dependency

Research indicates that vendor lock-in impacts cloud computing migration from multiple business perspectives, creating costs that extend far beyond obvious switching expenses. The financial implications accumulate across every aspect of cloud operations, often in ways that only become apparent during crisis situations.

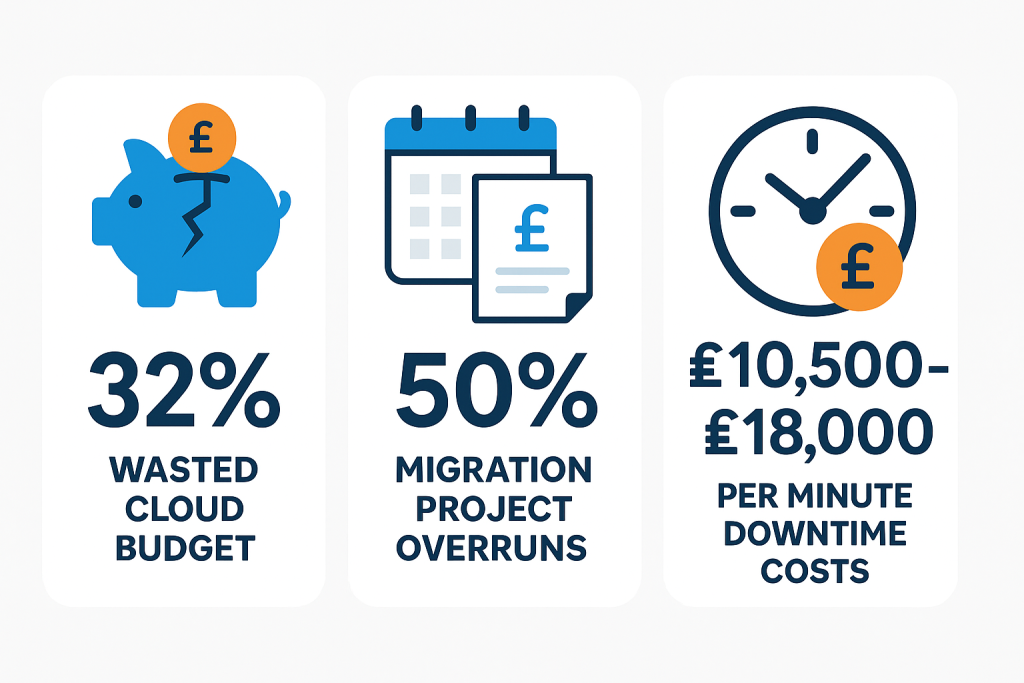

Studies demonstrate that 32% of cloud budgets go to waste due to lack of optimisation and vendor lock-in constraints, while migration projects frequently exceed budgets by 50% and timelines by 75% due to inadequate planning for dependency extraction.

Consider the business continuity implications: unplanned IT downtime averages £10,500 per minute for typical enterprises, rising to £18,000 per minute for large organisations. These figures underscore why single-vendor dependencies create such substantial business risks. When AWS experienced major outages in recent years, entire sectors of the digital economy ground to a halt, highlighting the systemic risks of over-concentration.

However, the economic case for avoiding lock-in extends beyond risk mitigation to tangible competitive advantages. Organisations implementing multi-cloud strategies report average cost reductions of 30% through strategic provider selection and improved negotiating positions. Companies with credible multi-cloud alternatives achieve 15-25% better pricing in contract renewals, demonstrating how exit options translate directly into financial benefits.

Perhaps most compellingly, comprehensive ROI studies show 304% returns over three years for hybrid cloud management strategies, with payback periods of less than six months. These returns reflect not just cost optimisation but enhanced operational productivity, with 75% reduction in deployment times and 25% overall savings on cloud spending through strategic multi-provider approaches.

The Technical Revolution Enabling Freedom

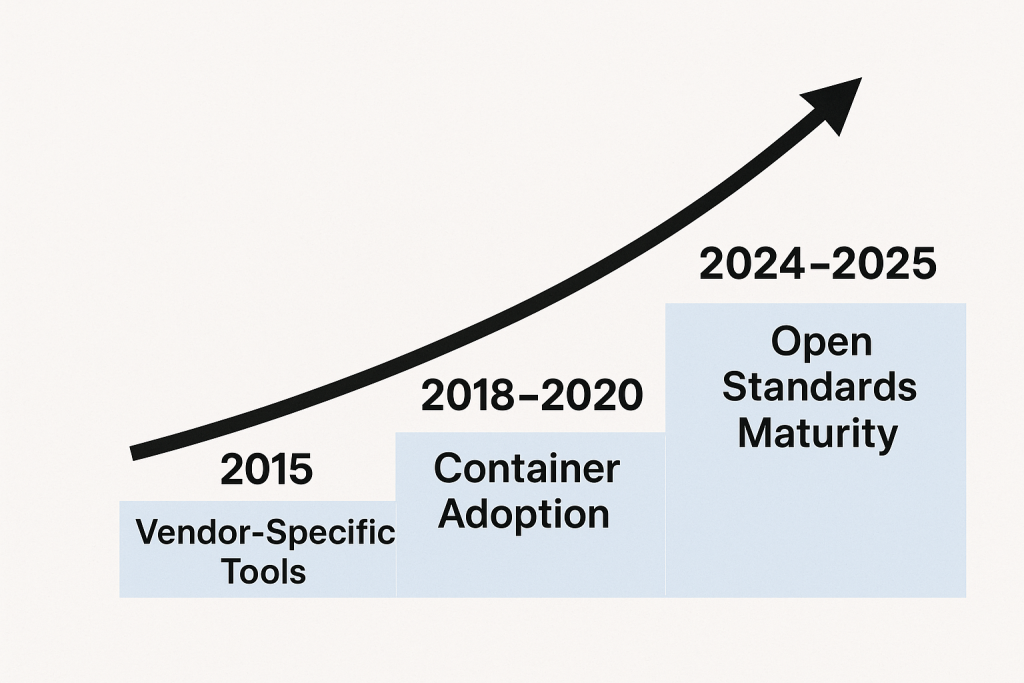

The emergence of cloud-native technologies represents the most significant development in achieving cloud portability since the industry’s inception. Kubernetes has achieved an extraordinary 84% adoption rate as of 2023, establishing itself as the de facto standard for container orchestration across all major providers. This universal adoption creates genuine workload portability that was unimaginable just five years ago.

Think of Kubernetes as the lingua franca of modern cloud computing—a universal translation layer that enables applications to run consistently across different cloud environments. The Cloud Native Computing Foundation (CNCF) landscape demonstrates remarkable maturation, with graduated projects providing production-ready alternatives to proprietary solutions.

OpenTelemetry grew 35% in 2023, standardising observability data collection across cloud environments, while projects like Cilium, Falco, and Helm provide vendor-neutral alternatives for networking, security, and application management. These aren’t experimental technologies anymore, they’re enterprise-grade solutions being adopted by the world’s most demanding organisations.

Platform engineering represents the cutting edge of this transformation. The multi-cloud management market has experienced explosive growth, reaching £10 billion in 2023 with a projected compound annual growth rate of 23.8%. Leading platforms like Flexera One, IBM Turbonomic, and VMware Tanzu provide sophisticated capabilities for managing workloads across multiple cloud environments while maintaining consistent security, compliance, and operational procedures.

The effectiveness of these platforms, however, depends heavily on architectural decisions made during initial cloud adoption. Organisations that prioritise open standards and container-based architectures from the outset find multi-cloud platforms significantly more valuable than those attempting to retrofit legacy cloud deployments.

Regulatory Earthquake Reshapes the Landscape

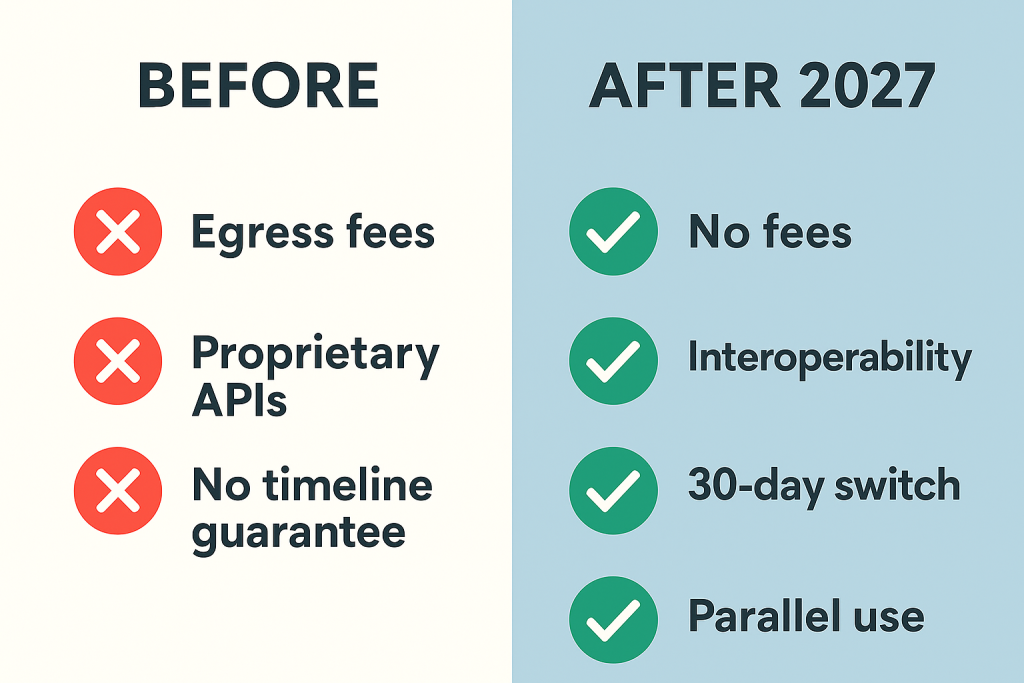

The European Union has effectively weaponised regulation against cloud vendor lock-in practices, creating the most significant external pressure on industry practices in cloud computing’s history. The Digital Markets Act, fully effective since March 2024, has already resulted in enforcement actions against major technology companies, while the Data Act’s provisions will fundamentally transform cloud switching economics by January 2027.

The Data Act’s switching provisions are particularly revolutionary. From January 2027, cloud providers will be prohibited from charging switching fees or data egress charges, with mandatory support for customer migration processes. Providers must implement interoperability specifications, offer parallel cloud usage during transitions, and complete customer switches within 30-day timelines.

This regulatory pressure has already prompted significant policy changes from major providers. Both AWS and Google Cloud eliminated egress fees for customers migrating to other providers in 2024, following competitive pressure and regulatory scrutiny. Microsoft Azure subsequently announced similar policies, demonstrating how regulatory frameworks can rapidly reshape industry practices.

Government initiatives like Germany’s Gaia-X, despite facing implementation challenges, have evolved from sovereignty-focused ambitions to practical federated data infrastructure supporting over 180 data spaces across multiple sectors. These developments signal a fundamental shift in how governments view cloud competition and digital sovereignty.

Lessons from the Trenches: Success and Catastrophic Failure

Real-world experiences provide the most compelling evidence for strategic approaches to cloud vendor relationships. The contrast between success stories and high-profile failures illuminates critical decision points that determine long-term outcomes.

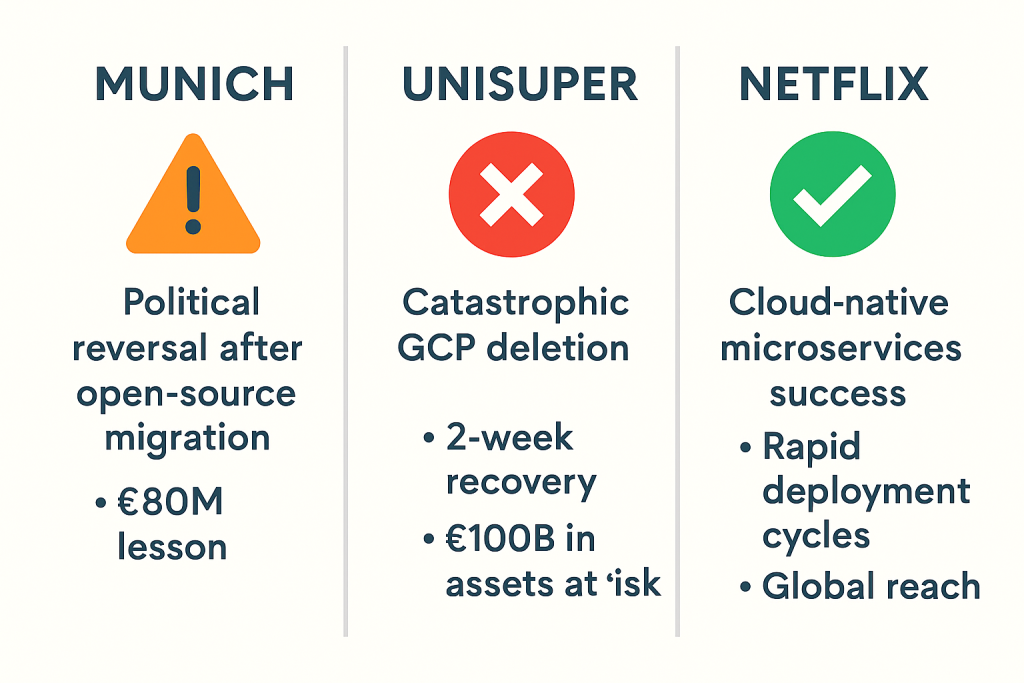

Munich’s £80 million lesson offers a sobering reminder that vendor lock-in extends beyond technology to encompass skills, processes, and organisational culture. Despite investing £23 million to migrate 15,500 desktop computers from Microsoft Windows to open-source alternatives, the city ultimately reversed course in 2017, spending an estimated £100+ million to return to Microsoft technologies. The reversal wasn’t primarily technical, project leaders characterised the decision as “political rather than technical”.

The UniSuper catastrophe of May 2024 provides a stark reminder of single-vendor risks. Google Cloud accidentally deleted the entire private cloud subscription of Australia’s largest superannuation fund, affecting £100 billion in managed assets and 647,000 members. Despite geographic redundancy across two Google Cloud regions, both locations were deleted simultaneously due to a provider-level configuration error. The two-week recovery period was only possible because UniSuper maintained independent third-party backup systems outside Google Cloud.

Netflix demonstrates the gold standard for strategic cloud adoption. Rather than lifting and shifting existing applications, Netflix rebuilt virtually all technology as cloud-native microservices, ultimately operating over 1,000 independent services across multiple AWS regions. This architectural approach enabled the company to achieve unprecedented global scalability while maintaining operational flexibility. The result: deployment cycles shortened from quarterly updates to multiple releases per day, while achieving global reach supporting billions of hours of content monthly.

Provider Evolution Under Pressure

Major cloud providers are responding to lock-in criticism and regulatory pressure with significant policy changes and enhanced interoperability efforts. These developments reflect both defensive responses to antitrust investigations and strategic positioning for a more competitive future.

The elimination of egress fees represents the most visible policy shift, with AWS, Google Cloud, and Microsoft Azure all removing data transfer charges for customers migrating to competitors. However, these policies typically require complete account closure within 60-day periods, limiting their practical value for organisations seeking gradual migration strategies.

More significant are ongoing improvements to data export tools, migration services, and compatibility layers. Google Cloud maintains the strongest commitment to open source principles, with approximately 10% of Alphabet’s workforce contributing to open source projects. AWS’s open source strategy focuses heavily on database and container technologies, employing six PostgreSQL committers and contributing significantly to Kubernetes ecosystem projects.

Despite these contributions, core proprietary services remain largely incompatible across providers. Database services, serverless platforms, and AI/ML tools continue to employ vendor-specific APIs and data formats that resist standardisation efforts.

Practical Strategies for Cloud Freedom

The convergence of regulatory pressure, technological maturation, and business demand creates unprecedented opportunities for organisations to achieve genuine cloud flexibility. Success requires strategic architectural decisions, investment in cloud-native capabilities, and sophisticated contract negotiation.

Container-first architecture provides immediate portability benefits. Organisations prioritising containerised applications with Kubernetes orchestration gain immediate portability benefits across all major cloud providers. The key lies in avoiding provider-specific container services and maintaining discipline around open standards adoption. The emergence of standardised container runtimes and the Open Container Initiative (OCI) specifications ensures that containerised workloads can run consistently across different environments.

Platform engineering creates sustainable competitive advantages. The fastest-growing trend in cloud-native adoption involves building Internal Developer Portals using tools like Backstage that abstract cloud complexity from development teams. Organisations implementing platform engineering approaches report 75% reduction in deployment times and significantly improved developer productivity while maintaining cloud portability.

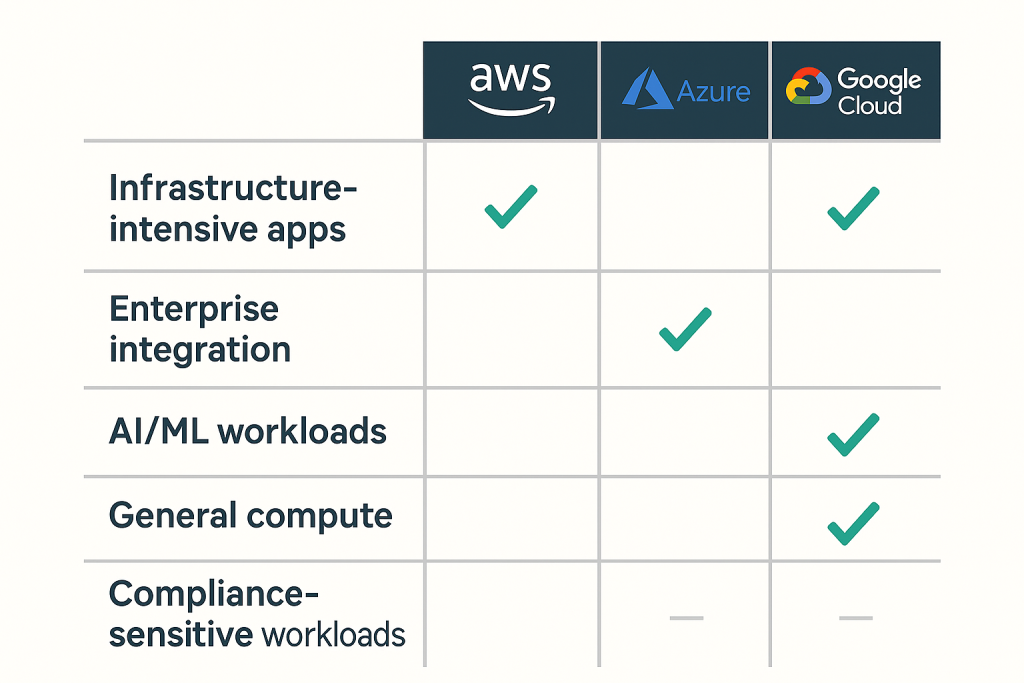

Multi-cloud strategies demand sophisticated management but deliver measurable benefits. The most successful implementations focus on workload-appropriate provider selection rather than redundant services across multiple clouds. For example, using AWS for infrastructure-intensive applications, Azure for enterprise integration requirements, and Google Cloud for AI/ML workloads.

Looking Forward: The Competitive Cloud Ecosystem of 2027

Gartner predicts that cloud will become a business necessity by 2028, with organisations requiring strategic flexibility to adapt to rapidly changing market conditions. The transformation of cloud vendor lock-in from accepted practice to competitive disadvantage represents one of the most significant shifts in enterprise technology strategy since the industry’s inception.

The success stories demonstrate that organisations approaching cloud adoption as comprehensive business transformation, rather than technology migration, consistently achieve superior outcomes while avoiding vendor dependency risks. Companies like Capital One that invested in cloud-native transformation have achieved dramatic improvements in deployment velocity, operational efficiency, and innovation capacity.

By 2027, when the EU Data Act’s switching provisions take full effect, the cloud computing landscape will likely feature genuine interoperability, standardised migration processes, and competitive pricing models that prioritise customer value over vendor control. The combination of regulatory requirements for cloud portability and technological maturation of open standards creates unprecedented opportunities for organisational agility.

What strategic decisions is your organisation making today to ensure cloud freedom tomorrow? The tools, technologies, and regulatory frameworks are aligning to support genuine choice and flexibility. The question isn’t whether vendor lock-in will become obsolete, it’s whether your organisation will be positioned to benefit from its demise.

The revolution in cloud freedom represents more than technological evolution; it enables organisations to focus on business value creation rather than vendor relationship management. This transformation promises to unlock the cloud’s full potential for driving innovation, operational efficiency, and competitive advantage across every sector of the global economy.